Weather: The US is seeing above-average to near-normal precipitation across most regions, with parts of the West trending below average. Forecasts point to wetter conditions across the Northern Plains and Canada over the next two weeks. Meanwhile, talk of potential harvest delays in Russia is increasing, though it’s not yet having a meaningful impact on markets.

Markets: President Trump’s latest demand, in the form of yet another tariff threat against Russia, triggered another market drop and increased trading uncertainty. Managed money traders continued to add to their long positions in the CBOT last week. The one bright spot in an otherwise red market was corn, which bounced off its recent lows.

Australian Day Ahead:

Futures are down, while the AUD held steady. Markets were relatively unchanged in the East yesterday, but fell 5–10 in the West.

Offshore

Wheat

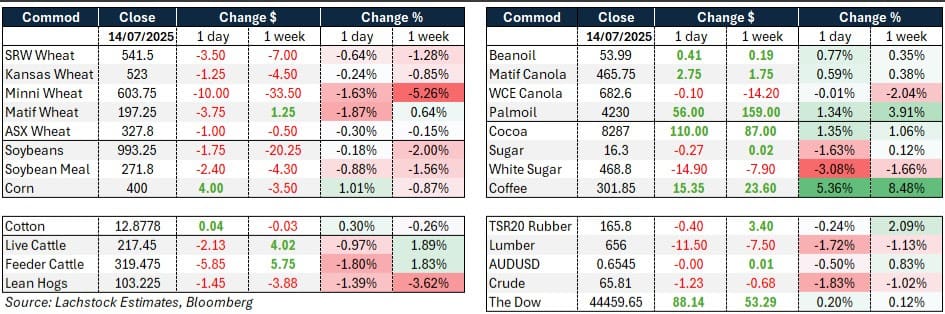

US wheat futures continued to decline overnight: Spring wheat (MWU) fell 10c, hard red winter (KWU) down 1.25c, and soft red winter (WU) down 3.5c. Paris MATIF fell €3.75 while Russian cash held steady.

There is ongoing concern around Russia: harvest delays, poor farmer selling, and a tight FOB market could support prices, but US futures remain cautious until clear demand surfaces.

Since the season kicked off on July 1, Ukraine has exported 486,000 tons of grain, a sharp decline from roughly 2 million tons at the same time last year, according to the agriculture ministry’s Monday update.

Other grains and oilseeds

US corn markets remain under pressure, despite a relatively supportive USDA update. The weakness may stem from growing speculation that crop conditions are not as strong as previously believed, with photos of potential damage circulating among traders. Overnight, EuroNext canola rose by €1.25 (ENC), while corn followed suit, gaining 4 points from the previous close. Soybean oil also experienced an uptick, although soybean meal and crude oil both trended lower.

US biofuel producers are expected to use more than half of the country’s soybean oil production in the future. This growth will likely be driven by upcoming federal policies, including tighter restrictions on foreign biofuel imports and stricter blending mandates.

Macro

It looks like Trump may have crossed the picket line, pledging top-of-the-line supplies for Kyiv and threatening to impose 100 percent tariffs on Russia if it does not sign a ceasefire deal. With secondary tariffs on countries trading with Russia that continue to purchase Russian oil and gas.

Letters were also sent to 14 countries, including Japan and South Korea, notifying them of new tariffs set to take effect on August 1, 2025. These tariffs are part of a broader strategy to address trade imbalance.

Today’s key focus is the US CPI release for June, which may show some signs of tariff pass-through. However, the figures could still be distorted as businesses continue to draw down inventory purchased before the tariffs took effect.

Australia

New canola values remained mostly unchanged over the week, with Port Kembla and Melbourne at A$811 track. Albany and Kwinana were both at $860 for CAN1.

NSW wheat showed a slightly firmer tone coming out of the weekend. Track values improved marginally, with some asset owners seeking specific sites on rail. Growers are gradually releasing residual unsold grain, though not in volumes large enough to flood the market.

Overnight rainfall was minimal, with VIC and SWA receiving 5–15mm. However, the VIC Mallee once again missed out—seemingly the Bermuda Triangle of rainfall.

Northern NSW is set to receive more rain, according to the 8-day forecast. Some areas haven’t seen rainfall in over a month, despite large standing crops in the region.

Markets appear to be in a holding pattern as farmers adopt a wait-and-see approach, seeking greater confidence before making moves. The school holidays may also be playing a role, with buyers hesitant to push aggressively during this period.

Please find the link to the article.

![]()