Weather

Cold risk is building across the Black Sea, with Ukraine particularly exposed due to limited snow cover and forecasts for temperatures as low as minus 30°C, while Russian logistics continue to be hindered by winter conditions.

Markets

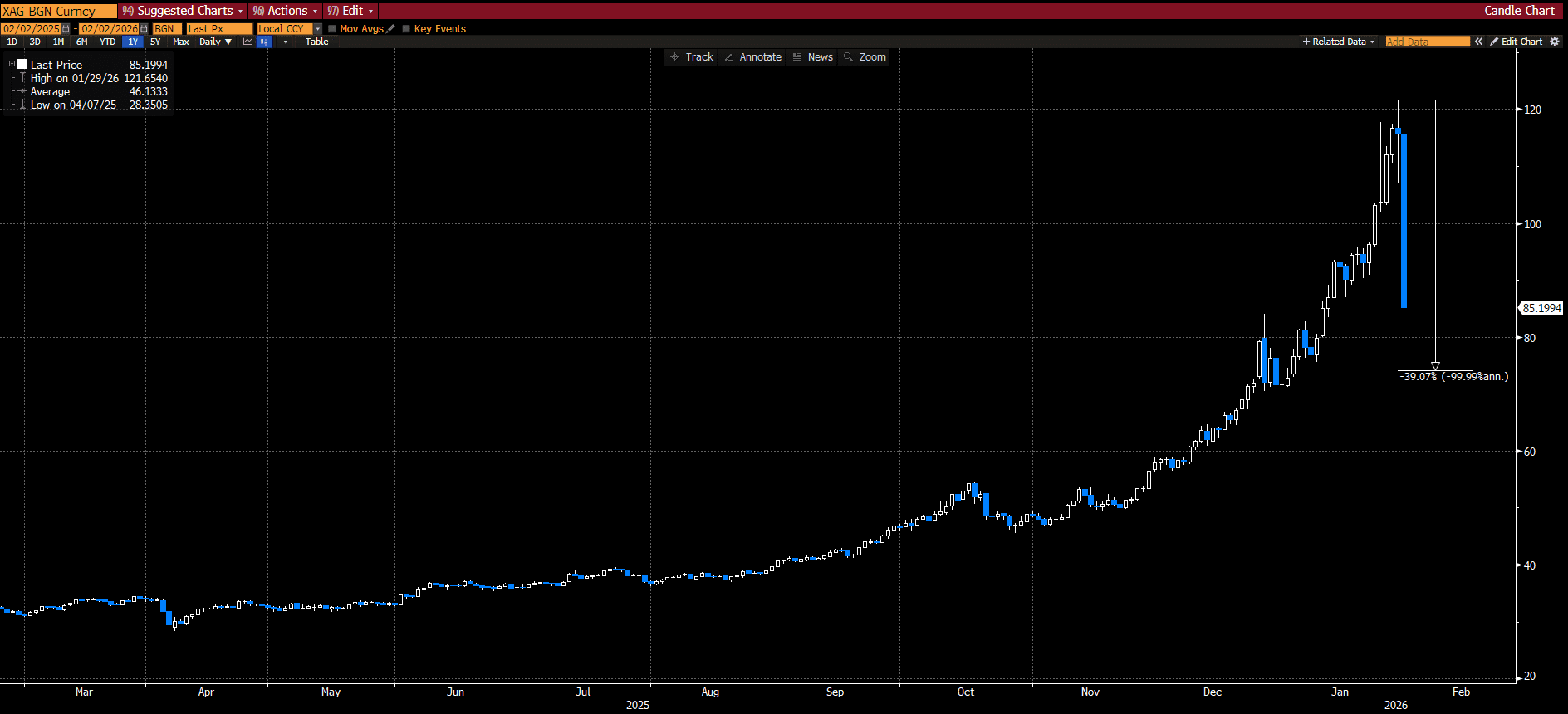

Absolute carnage in the precious metal pits with Silver leading the way lower. Walsh is an interesting choice to be head of the Fed – previously, when he was a Fed Governor he was aggressive on inflation and slow to cut rates. More recently however it has been said he is more open to lowering rates to maintain momentum. One thing is, he wants a small balance sheet which means the supply of bonds could increase which practically could support the USD, even if they are cutting rates.

Australian Day Ahead

Should be a little quieter today – AUD adding some support but growers now maybe focusing on marketing some old crop given school holidays are over.

Pockets of demand driven by export accumulation should still be a feature.

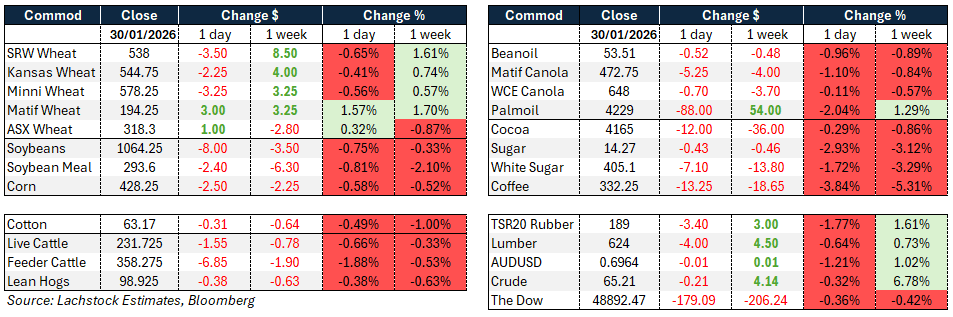

Wheat

- Chicago -3.5c, Kansas -2.25c, Matif -3.25c

- Wheat saw modest losses into the weekend, though Chicago and KC both managed fresh monthly highs before fading as a sharp selloff in gold and silver dragged broader risk sentiment lower.

- Spreads remained firm in Chicago and KC with delivery economics keeping focus on WHK, which settled at -8c and remains on track for potential contraction with only a modest average gain needed over the remaining sessions.

- Matif was relatively supported, aided by currency moves and talk of French wheat pricing into Morocco, as well as its competitiveness as a feed grain versus barley and corn.

- EU data showed slightly higher total grain output but lower soft wheat production and reduced export expectations, reinforcing the idea that supply-side risks remain uneven across regions.

- US winter wheat cold damage remains uncertain, with estimates suggesting 15–20% of the crop may be at risk in areas lacking snow cover, though the full impact may not be clear for several weeks.

Other Grains and Oilseeds

- Corn -2.5c, Soybeans -8c, Matif canola -5.25

- Corn and soybeans led a broader grains pullback, with markets increasingly focused on oversupply risks.

- Corn briefly traded higher before a macro-driven selloff took hold, with no fresh demand news and Argentine weather forecasts turning more favourable.

- Soybeans came under heavier pressure as expectations for a massive Brazilian crop dominated sentiment, with production estimates pushing toward record territory and export prices expected to soften further.

- Even potential losses in Argentina were viewed as manageable so long as Brazil delivers near-180+ million tonnes.

- Canola ended a choppy session slightly lower, capped by weakness in the Chicago soy complex and softer veg oils, though a weaker Canadian dollar provided some underlying support to crush margins and exports. Canadian export pace remains well behind last year.

- Palm oil also slipped on profit-taking, snapping a short run of gains, while soymeal and soyoil weakened, pulling crush margins lower.

- China has clearly pivoted back to Brazilian supply after recent US purchases, reinforcing the sense that South American availability will dominate oilseed trade flows in coming months.

- Tight US cattle supplies remain a longer-term supportive backdrop for feed demand, but for now grain markets remain hostage to grower selling behaviour, rolls and first notice dynamics rather than fundamental shocks.

Macro

- AUD sub 0.70, Dow lower, Crude down nearly 1%

- Macro conditions were a key drag on commodities, led by a historic collapse in precious metals.

- Gold and silver suffered violent selloffs as the US dollar strengthened following President Trump’s nomination of Kevin Warsh as the next Fed chair, triggering margin hikes and forced liquidation across metals and related equities.

- The surge in the dollar weighed broadly on risk assets and helped unwind earlier geopolitical risk premiums.

- Oil prices fell on signs the US may engage Iran diplomatically, even as rhetoric escalated sharply with Iran’s leadership warning of a potential regional war if attacked.

- Markets appear torn between rising geopolitical tension and the perception that actual supply disruptions may yet be avoided.

- US political uncertainty also lingered as lawmakers worked to avert a government shutdown.

- Overall, macro volatility dominated price action, reinforcing the sense that grains and oilseeds remain vulnerable to cross-asset moves despite localised weather and supply risks.

Local

- Bids ended the week steady in the west of the country with canola at A$775 and GM $685. Wheat was $321 and barley $320 FIS Albany.

- Through the east of the country canola was $749, wheat $322 and barley $304 track Geelong.

- Hot, dry conditions combined with slow grower selling saw delivered wheat and barley markets continue to trickle higher across both southern and northern regions.

- Sorghum lost around $10 over the past week, pressured by increased grower selling and a firmer AUD pulling bids back.

- Heat, rather than demand, is disrupting eastern cattle markets, with January sale-yard throughput hit by extreme temperatures and public holidays, while processors have largely maintained kills by shifting movements to early morning and dusk. Slaughter remains slightly ahead of last year, with EYCI, NYCI and Feeder Steer broadly in line with early-2025 levels after a modest pullback this week.

Click here to read the full report.

![]()